Are you considering converting your traditional IRA to a Roth IRA, but worried about the potential impact on your Medicare premiums? You're not alone. Many retirees are facing this dilemma, and it's essential to understand the relationship between Roth conversions and Medicare increases. In this article, we'll delve into the details and provide you with practical solutions to minimize the financial blow.

Understanding the Connection Between Roth Conversions and Medicare Increases

When you convert a traditional IRA to a Roth IRA, you're essentially transferring funds from a tax-deferred account to a tax-free account. This conversion is considered taxable income, which can increase your Modified Adjusted Gross Income (MAGI). Unfortunately, a higher MAGI can lead to higher Medicare premiums, particularly for Part B (outpatient services) and Part D (prescription drug coverage).

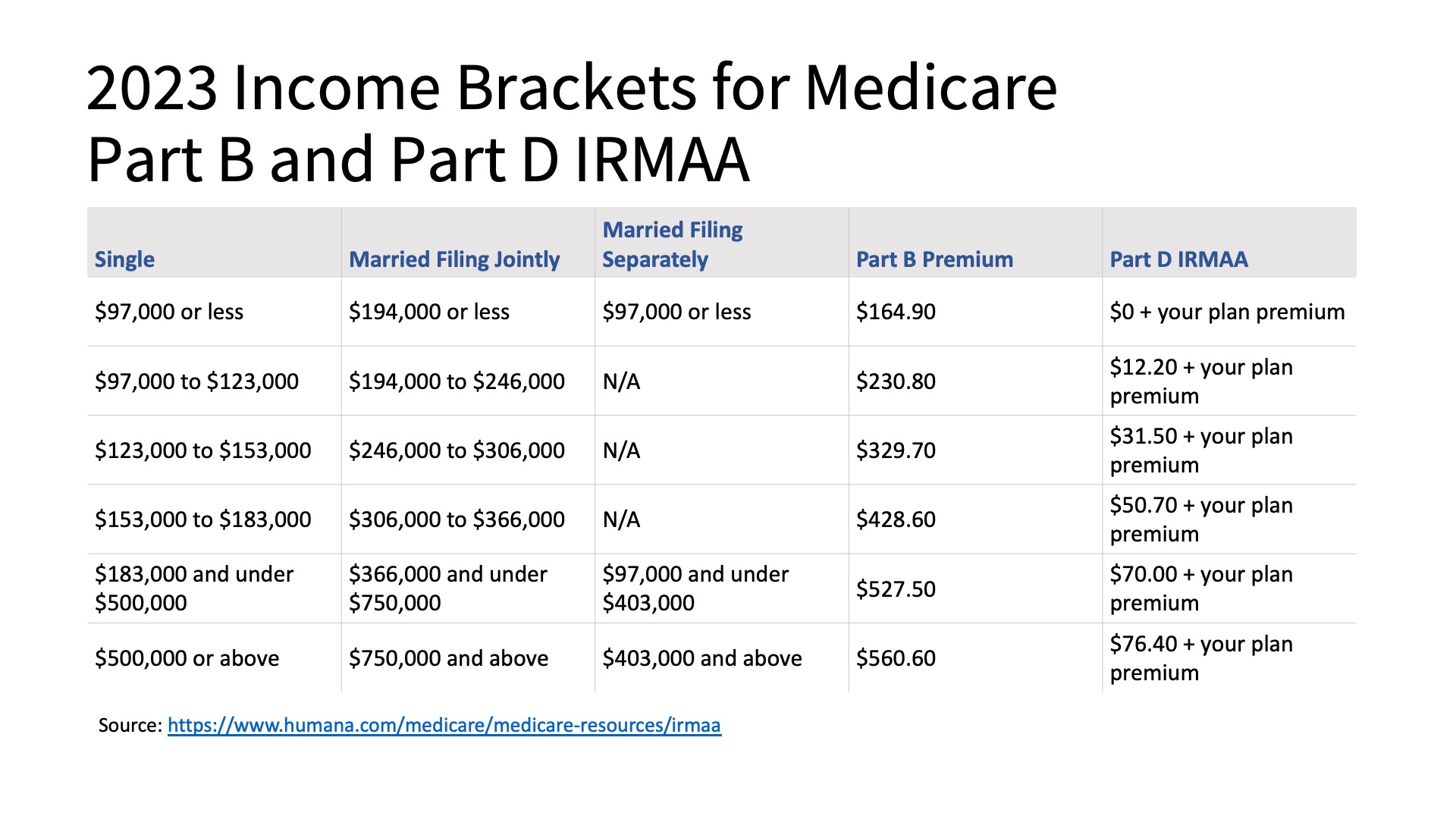

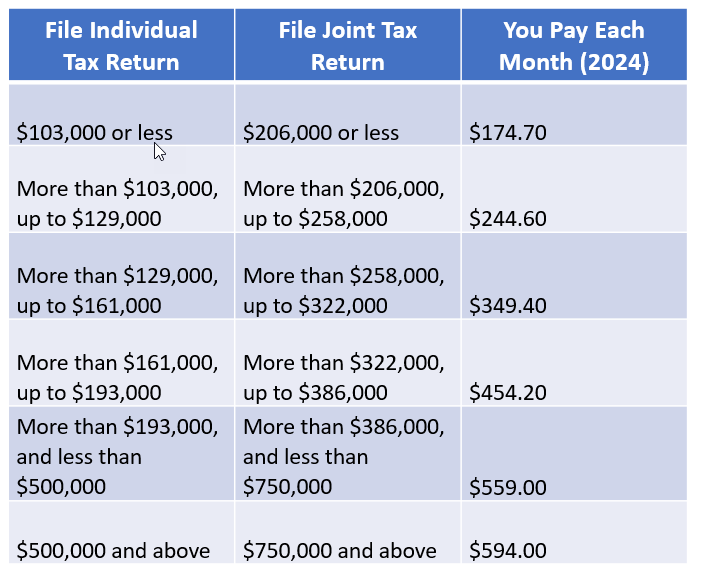

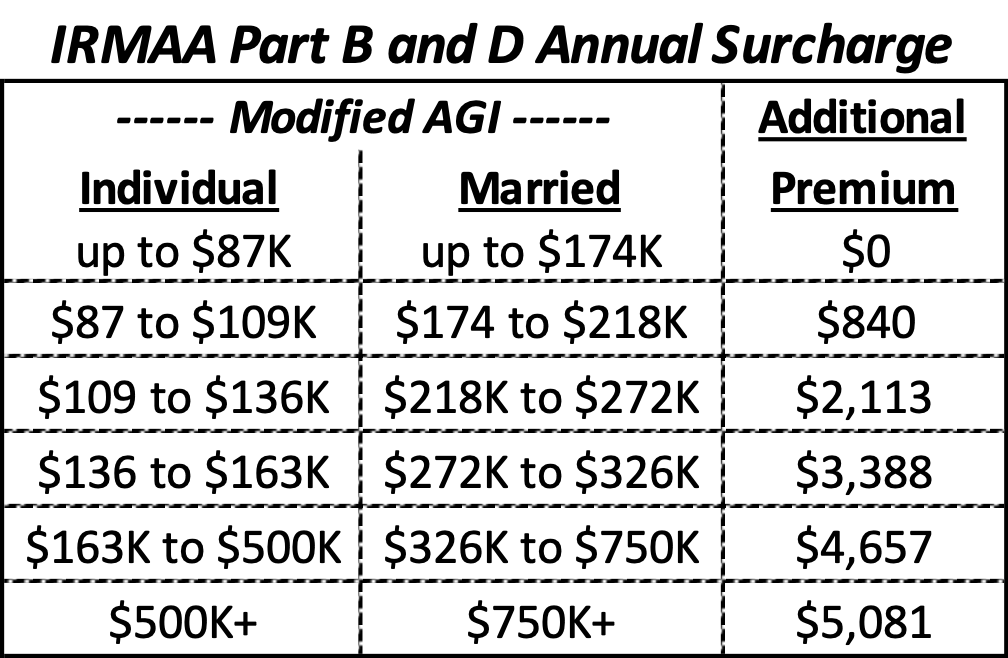

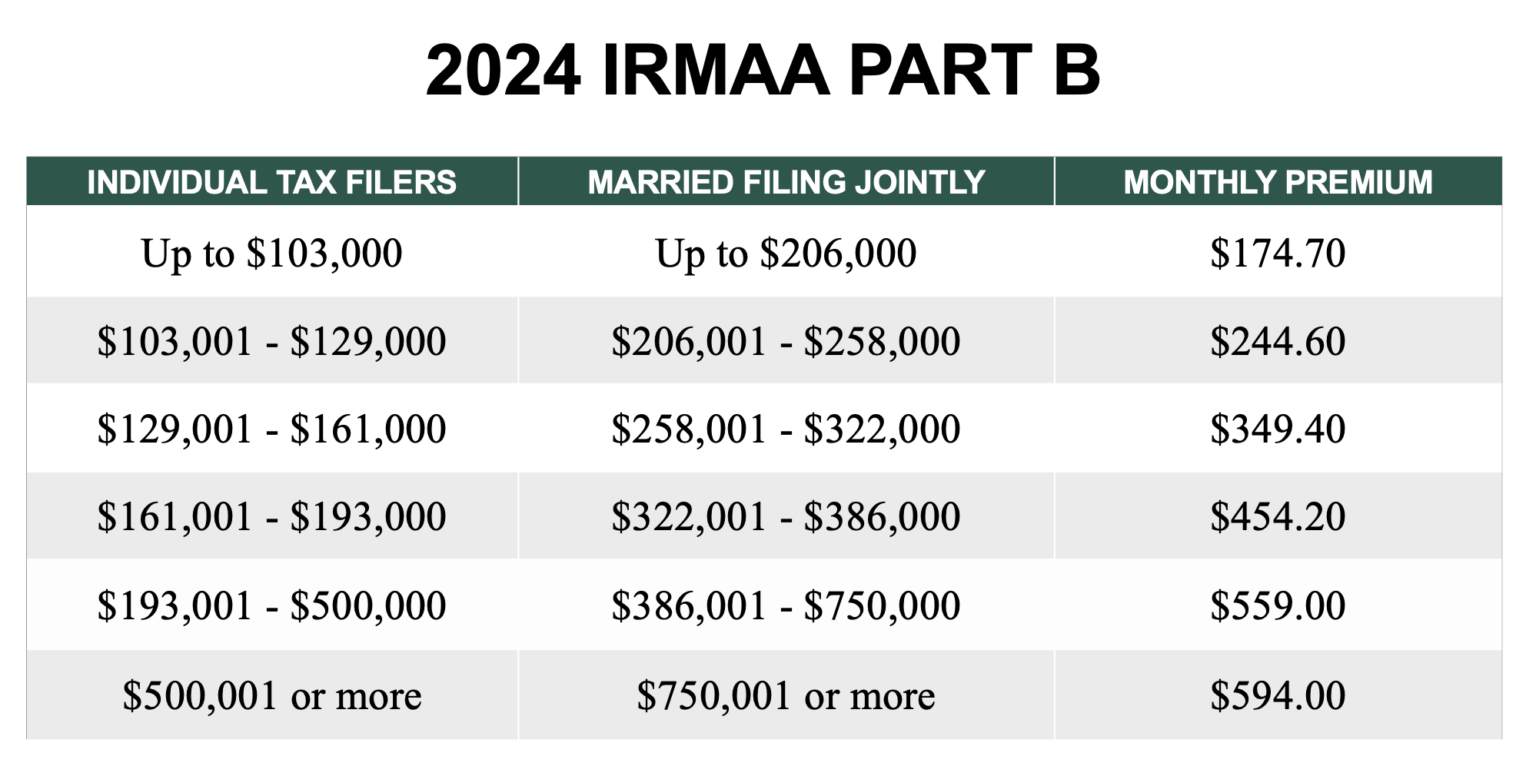

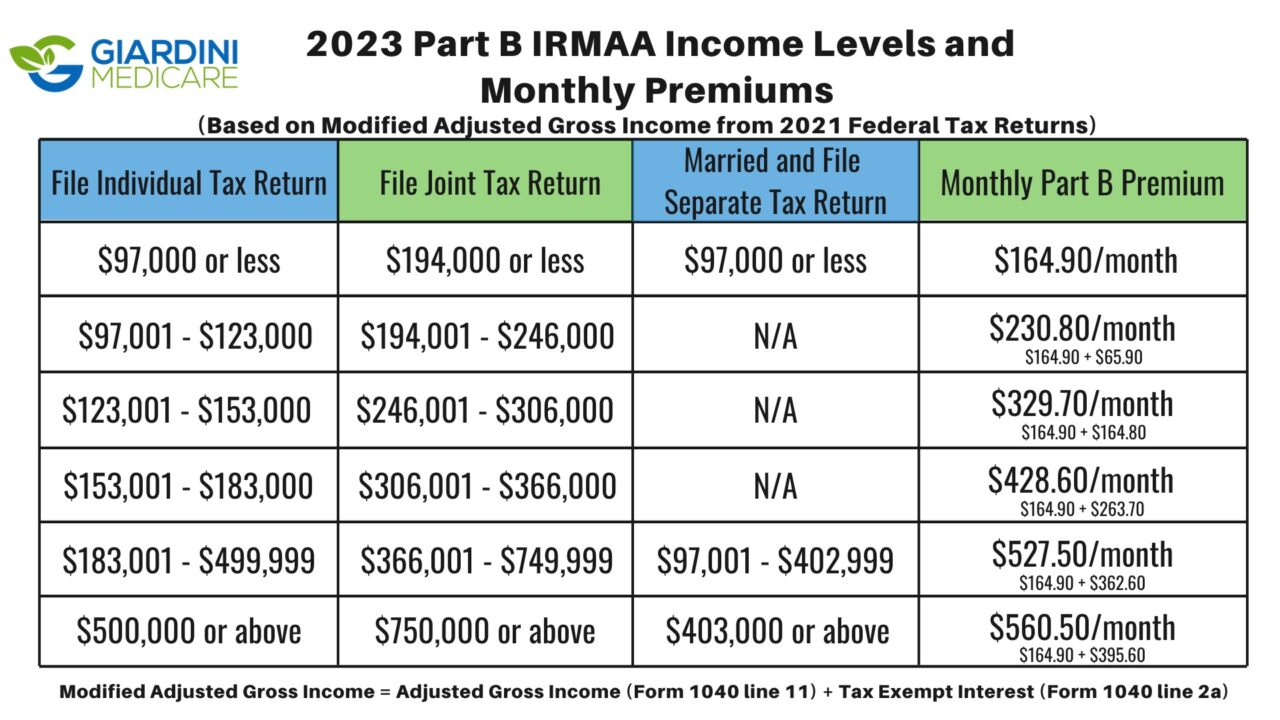

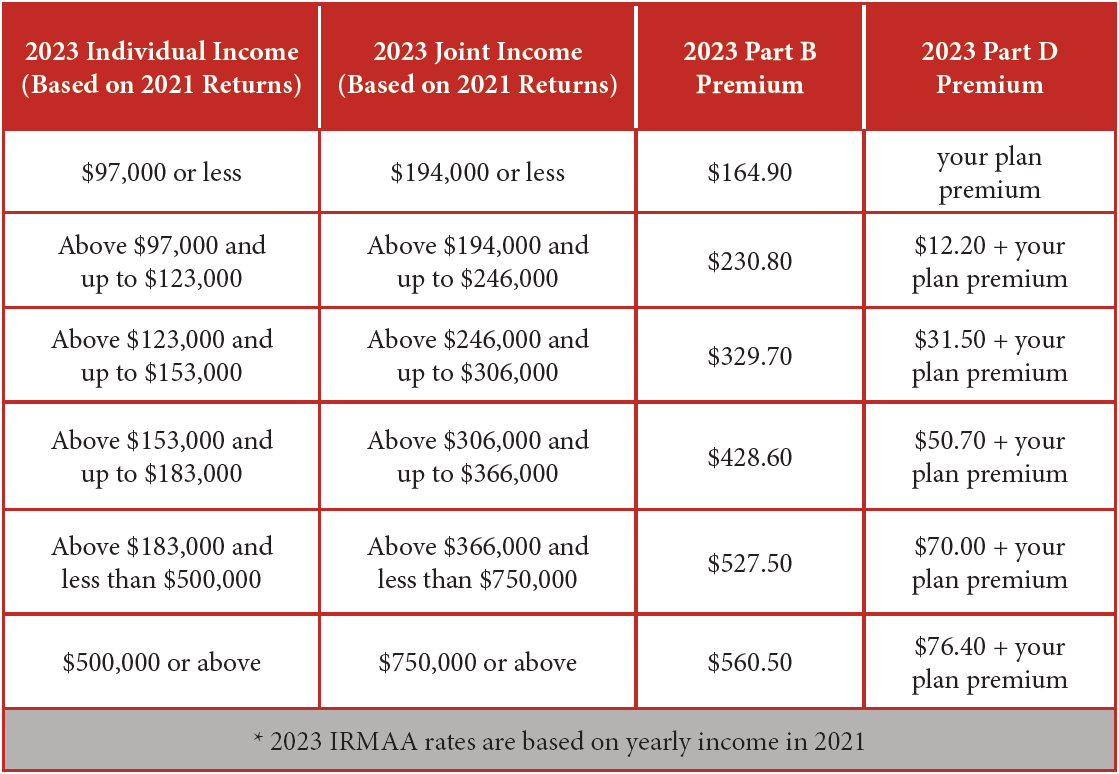

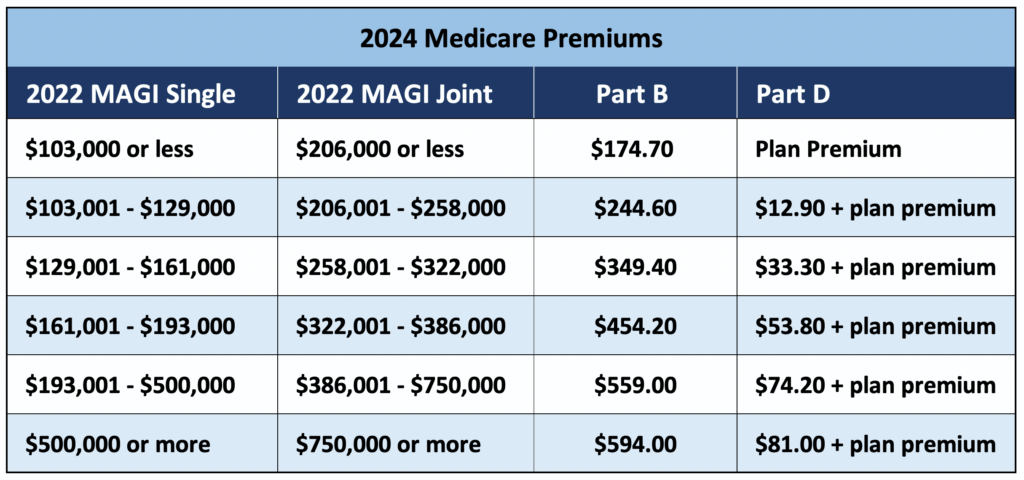

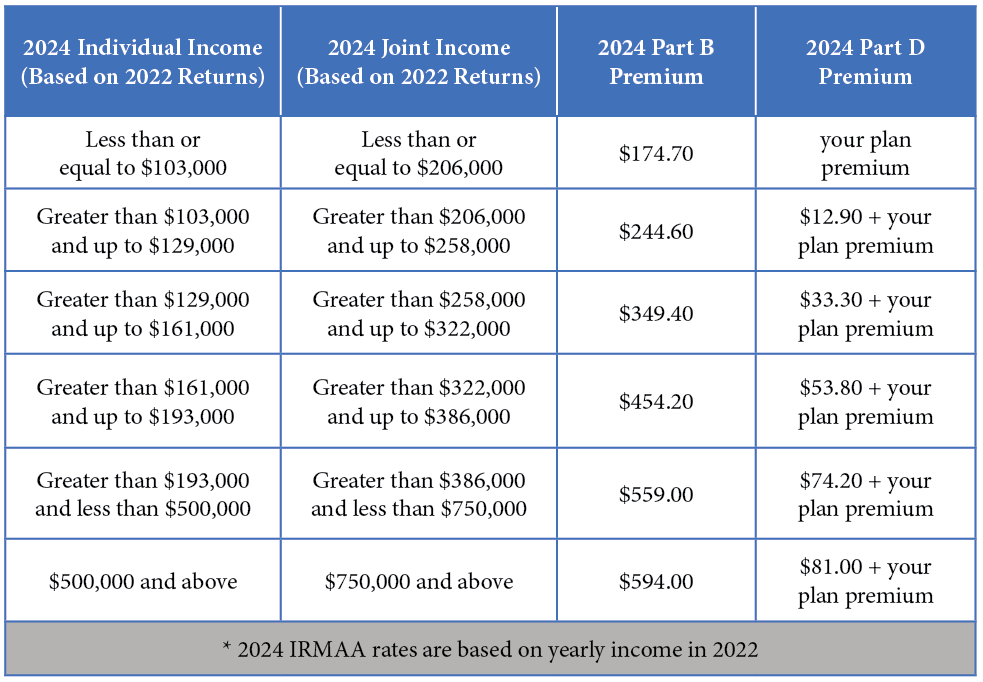

The Medicare premium increase is based on the Income-Related Monthly Adjustment Amount (IRMAA), which is calculated using your tax return from two years prior. For example, your 2022 tax return will determine your 2024 Medicare premiums. If your MAGI exceeds certain thresholds, you'll be subject to higher premiums.

How to Minimize Medicare Increases Due to Roth Conversions

While it's impossible to avoid the tax implications of Roth conversions entirely, there are strategies to minimize the impact on your Medicare premiums:

1.

Space out your conversions: Instead of converting a large amount in one year, consider spreading the conversions over several years. This can help keep your MAGI lower and reduce the likelihood of triggering higher Medicare premiums.

2.

Consider a partial conversion: If you have a large traditional IRA, you might not need to convert the entire amount. Converting a smaller portion can help minimize the tax impact and reduce the potential Medicare premium increase.

3.

Factor in other income sources: If you have other sources of income, such as a pension or rental properties, consider how these will impact your MAGI. You may be able to adjust your income or expenses to offset the effects of the Roth conversion.

4.

Consult a financial advisor: A professional can help you navigate the complex tax and Medicare landscape, ensuring you make informed decisions about your retirement accounts and minimize any potential increases in Medicare premiums.

Roth conversions can be a valuable tool for managing your retirement income and minimizing taxes. However, it's essential to consider the potential impact on your Medicare premiums. By understanding the connection between Roth conversions and Medicare increases, and implementing strategies to minimize the effects, you can make informed decisions about your retirement planning. Remember to consult with a financial advisor to ensure you're making the best choices for your individual circumstances.

By taking a proactive approach to managing your retirement income and Medicare premiums, you can enjoy a more secure and sustainable retirement. Don't let the fear of Medicare increases hold you back from making the most of your retirement savings. With careful planning and expert guidance, you can navigate the complexities of Roth conversions and Medicare, ensuring a brighter financial future.

Word count: 500

Note: This article is for general information purposes only and should not be considered as professional advice. It's always recommended to consult with a financial advisor or tax professional to determine the best course of action for your individual circumstances.